Open Government for Dummies: Accountability

We explain what accountability entails in Open Government and offer examples of good practices.

Available in:

By Laura Tamia Ortiz Chaves. Published: July 2021.

In previous posts, we approached Open Government. We talked about its definition, its pillars and reviewed what transparency and participation mean in this form of governance. Here we will talk about accountability.

What does accountability mean?

Accountability is probably the least discussed pillar of Open Government. ECLAC says that accountability “consists of the existence of rules, regulations, and mechanisms that guide the behavior of elected authorities and officials in the exercise of public power and the expenditure of fiscal resources. These rules should include requirements that decisions be fully reasoned and justified with all information made available to the public. That there be protection for whistleblowers and mechanisms to react to revelations of wrongdoing and irregularities.”

In other words, it is a set of tools, which allow the control and supervision of the action of rulers, civil servants, and private individuals who manage public money by other actors, such as citizens, other agencies, and international institutions. It aims to measure the performance and results of governments and guarantee the rights of citizens. These actions must be able to be carried out securely and with guarantees. The Transparency and Accountability Initiative (TAI) stresses the need for officials to be held accountable for their actions and redress when obligations and commitments are unmet. It proposes broadening the scope of those who should be held responsible for including civil society organizations.

How to be accountable?

Accountability processes can be very diverse and have different moments that depend on the involvement of the institution that performs it, citizen participation, and the consequences that the process itself may have. Some authors, such as Moore and Teskey (2006), identify three types of accountability concerning who demands compliance and carries out supervision. Thus, the horizontal model is the one that occurs within the entities or the State, i.e., when an institutional actor has the formal power to demand explanations and impose sanctions on another (we find here, for example, the exercises that are carried out before the control bodies). The second model, or vertical, occurs when citizens and civil organizations are the ones who demand accountability and exert pressure on the institution or actors in power. Although they cannot impose formal sanctions, there may be punishments in case of non-compliance, such as those related to reputation and lousy publicity (we find citizen monitoring or social audits, for example). The third model, the diagonal one, is a hybrid between the two previous ones. Institutions are accountable both internally and externally, and channels of communication and direct engagement with and for citizens are established. It is this latter model that Open Government seeks.

In a complete process, accountability would begin with creating rules, which establish the behavior expected of those who are accountable and the criteria by which they can be validly judged. After this, an investigation follows to clarify whether or not those responsible have fulfilled what is expected of them. Then, a process would be generated in which those responsible can defend their actions, answer questions and comments (positive or negative) about their management and explain themselves to the citizens. Finally, there would be a process of sanction or recognition for falling what is expected of them.

Without transparency, those in charge of supervision - institutional or civilian - cannot carry out the necessary investigation to determine compliance or non-compliance. Without the supervisor’s participation, if the process only depends on the supervised party, the aspects with less compliance will hardly be dealt with within defending the actions carried out. Likewise, to ensure the effectiveness and confidence of accountability, the standards required must be met by those who carry out the supervision. They have to be transparent, avoid political interference or possible co-optation, and that these bodies are independent, open to citizen involvement, and can listen and respond.

Open Government Standards: accountability

According to the Open Government Standards (2015), the Accountability standards are as follows:

- Codes of Conduct: Clear standards of behavior: There are norms and standards of behavior in public life, such as a code of conduct. It should be enforced by institutions guaranteeing the accountability and responsibility of elected and unelected public officials for their actions and decisions, ensuring that they avoid engagement in decisions or judgments affected by their private interests. Codes should also require public officials to keep an accurate and complete record of their actions.

- Conflict of Interest Prevention Mechanisms: That potential conflicts of interest in decision making are avoided through a clear regulatory and practice framework which ensures that public officials are not engaged in decisions where their judgment might be affected by their private interests.

- Assets Disclosure: An effective and transparent assets disclosure regime creates a framework under which illicit enrichment during public service can be prevented.

- Transparency and Regulation of Lobbying: That lobbying is subject to regulatory controls accompanied by sufficient transparency to ensure that the public has oversight of the influence of private or group interests in public decision-making.

- Whistleblower mechanisms and protections Standard: That there are channels by which public officials can reveal corruption, wrongdoing, mismanagement, or waste within government and that there are protections in place for those who raise the alert, whether they do so internally or by going public with the revelations. There should also be sanctions for failing to report wrongdoing.

- Procurement Transparency: There is complete transparency of the public procurement process to reduce the opportunities for corruption, ensure effective spending of public funds, and create a level playing field of business opportunities.

- Independent Enforcement Bodies: There exist independent bodies that oversee the exercise of public power; these can range from Ombudsman institutions to supervision of public services and public spending (audit offices) to oversight by the legislative and judicial branches.

Promoting accountability from civil society

At the beginning of 2021, the Open the Government initiative published the document “Accountability 2021”. It was drafted with more than 20 organizations and had recommendations addressed to the US Federal Government. It urges to restore accountability, create a persistent accountability plan over time, and promote transparency, citizen participation, ethics, and oversight.

What is interesting is that it identifies open government as a necessary basis for creating an accountable government. It is guided by eighteen principles and six categories (open government, ethics, balance of power, whistleblower protection, responsible government, and pandemic preparedness and response), which, although addressed to the US government, can be extrapolated, for the most part, to other countries. The first milestone of this initiative was to get the current US President Joe Biden to sign, on the first day of his term, an executive order on ethical commitments for the executive branch and other actions included in the recommendations.

Another striking example, in this case within Civil Society Organizations (CSOs), is the “Regional Civil Society Accountability Initiative”, which emerged in 2009 to promote transparency and accountability within civil society itself in Latin America. They have created the Global Standard for Accountability of Civil Society Organizations (CSOs) through a participatory process and offer free training for CSOs on the subject http://www.rendircuentas.org/campus/.

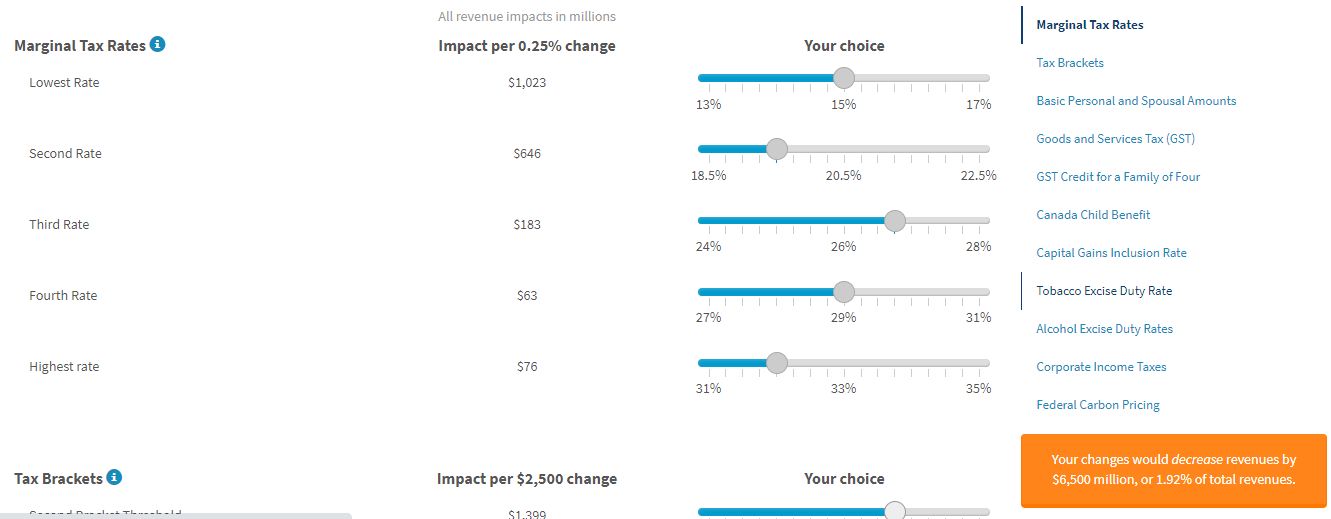

Finally, we find noteworthy the Canadian Parliamentary Budget Office’s “Ready Reckoner” tool. It allows citizens to calculate the potential revenue impacts of adjustments to various tax rates, credits, and brackets in the federal tax system. The agency for such information developed it in response to numerous requests received. http://www.readyreckoner.ca/

If you would like more information on this topic, we encourage you to subscribe to our Open Government newsletter and visit the following links:

- How do we define key terms? Transparency and accountability glossary

- Accountability Standards

- The CAR Framework: Capability, Accountability, Responsiveness. What Do These Terms Mean, Individually and Collectively?

- Accountability 2021

- Accountability in modern government: what are the issues?

- Executive Order on Ethics Commitments by Executive Branch Personnel

- Estándar Global para la rendición de cuentas de las OSC - Centro Virtual para la transparencia y la rendición de cuentas de la sociedad civil (ES)

- Guía de la OCDE sobre Gobierno Abierto para funcionarios públicos peruanos 2021(ES)

- Buenas prácticas de transparencia y participación ciudadana en los poderes legislativos de las Américas | PNUD en América Latina y el Caribe (ES)